The beginning of 2026 was truly the tale of two markets. Price bands and segments have been the primary differentiator in our marketplace these last few years; however, it looks like that has shifted to now include product type. The performance of single-family homes really stood out this quarter, with stronger activity than seen historically. Simultaneously, condo/townhome product had its worst quarter for closed sales since 2010 and general weakness across the board.

It is also quite apparent that the unique ski season experienced across the western United States played a role in the dynamics seen in Park City, with the low dose of snowfall reflected in market data.

How the 25’–26’ Winter Affected the Park City Real Estate Market

I have two primary thoughts on how this winter impacted our market:

- One of the biggest contingents of buyers and sellers in our resort market are move-up/move-down clients. These are going to be families that are growing and want a bigger space for vacations, or families that aren’t utilizing spaces quite as much. Friction tends to be felt while utilizing the property, and property owners were one of the groups that could cancel their ski trip with no penalty on accommodations, and therefore either didn’t feel the squeeze in a condo with new grandchildren, or the emptiness of a large house now that the kids are off to college or young adulthood. The result is less inventory and fewer buyers within the market.

- One of the most active portions of our market is the luxury segment, particularly when it comes to resort property. Of all the demographics that could afford to cancel their ski trip and eat the cost on their way to the beach, it was this segment. Without the proximity and experience in our market, potential purchases were either pushed to a later date or dropped.

Beyond the snowfall, the back end of Quarter 1 experienced unique market volatility due to geopolitical disruptions. Mortgage rates rose sharply, impacting the entry point to our market and overall affordability, and the equities market continues to experience significant fluctuations. These combine to create uncertainty, which is anathema to the real estate market; activity tends to pause with high levels of uncertainty. As you will see below, when looking at the top-down view of the Park City market, you can see that uncertainty comes out in the overall numbers.

Total Park City Market, All Property Types

- Median Sales Price:

- $2.246m, down 12.9% year-over-year, down 13.2 quarter-over-quarter

- Average Sales Price:

- $3.462m, down 5.3% year-over-year, down 9.6%, quarter-over-quarter

- Sold Properties:

- 196, down 14% year-over-year, down 31.7% quarter-over-quarter

- Sold Dollar Volume:

- $668m, down 19.2% year-over-year, down 26% quarter-over-quarter

- New Listings:

- 376, down 2.1% year-over-year, up 19.7% quarter-over-quarter

- Under Contract Properties:

- 241, down 5.5% year-over-year, up 12.1% quarter-over-quarter

- Total Active Inventory:

- 495, up 4.7% year-over-year

If this were the only picture of the Park City real estate market that you had, I doubt the feelings would be optimistic. Historically, there is always a drop in sold properties from Q4 to Q1, and while sold and under contract have dropped, inventory has not, showing a waning demand. However, when these numbers are broken out, we can see that there are two markets in play, and price is important but is taking a backseat to product type

Total Park City Market, Single Family Homes

- Median Sales Price:

- $3.525m, up 15.6% year-over-year, up 25.9% quarter-over-quarter. This is also a record high for median sales price in a quarter.

- Average Sales Price:

- $4.453m, down 4.4% year-over-year, up 17.7% quarter-over-quarter.

- Sold Properties:

- 106, on pace with quarter and annual production

- Sold Dollar Volume:

- $463m, accounting for about 70% of total sales volume, while unit sales only account for 54%

- New Listings:

- 179, on pace with quarter and annual production

- Under Contract Properties:

- 131, up 4.4% year-over-year, up 9.3% quarter-over-quarter

- Total Active Inventory:

- 210, down 13.9% year-over-year.

Single-family homes are in a class of their own this quarter, more insulated from the ebbs and flow of winter, and while more resilient to interest rate fluctuations, likely took advantage of the low rates we saw through January and February. From a price point perspective, single-family homes in our resort communities tend to be a premium price point relative to the condo/townhome product and appeal to a buyer who is more insulated from market fluctuations.

From a product type perspective, purchasers within our primary market aren’t looking at a single winter season or short-term market fluctuations as much; there is usually a life change that brought this purchase about. With inventory levels getting lower and sold/pended activity staying consistent, it tells me that demand is starting to increase and has the potential to outstrip supply if we don’t see increases to inventory. These numbers show a strong market for this product type. Below, you can see the other half of the equation.

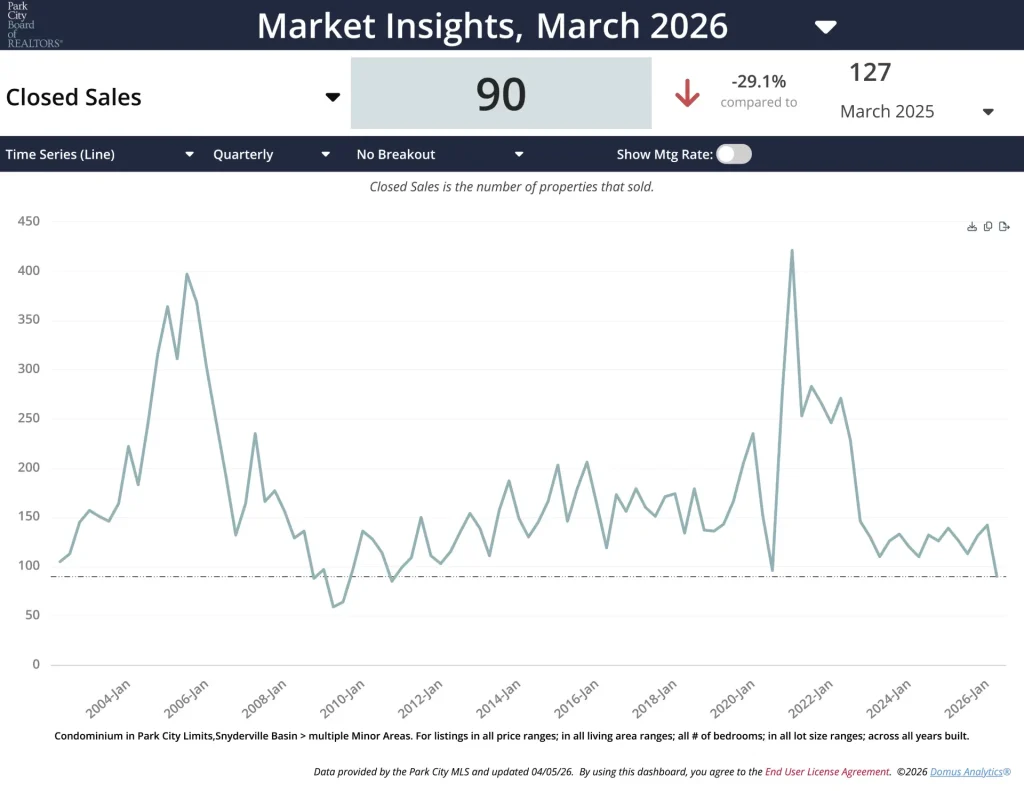

Total Park City Market, Condo/Townhomes

- Median Sales Price:

- $1.3m, down 7.8% quarter-over-quarter

- Average Sales Price:

- $2.3m, down 8.8% quarter-over-quarter

- Closed Sales:

- 90, down 36.6% quarter-over-quarter (This is also the lowest sales total for condo product since 2010.)

- New Listings:

- 197, on pace with quarter and annual production

- New Under Contract Properties:

- 110, down 16% year-over-year, up 13.4% quarter-over-quarter

- Active Inventory:

- 288, up 25.8% year-over-year.

A few notes on condo inventory: this current inventory level has only been seen twice in the last five years, once last July and again at the beginning of 2021. Given that our inventory peaks in July across all product types, it appears the market can become quite saturated this summer as we approach peak inventory levels. Additionally, Q4 of 2025 and Q1 of 2026 combine for one of the weakest consecutive quarters for condo sales since 2012.

Does this mean that condo/townhome inventory and product in Park City is a bad bet? Not necessarily, as with any generalized data, nuance exists and there are portions of our market and projects where inventory is in demand and commanding a premium. Condo/townhome product in the Park City market tends to exist across the echelon of pricing, but there is a significant concentration at the entry-level price points, which are the most sensitive to mortgage rate fluctuations.

With a weak season of rental bookings, the overall revenue these units produce dropped this year. It was a perfect storm of negative pressure points on this segment of the market. It certainly points to increased variability in sales price, which can help a buyer secure a better price, but also requires more diligence on the part of the buyer to ensure they are buying quality inventory. This could be a great opportunity for some buyers who can optimize for the current circumstances. With rising inventory and a reluctant buyer pool, the negotiating leverage is going to be with the buyer, giving you more choices at better prices than we have seen in quite some time.

The Park City market is going to continue to operate on its own unique fundamentals relative to the greater overall real estate market. Each neighborhood is truly a micro-market. If you’d like additional information or data on a specific area, please reach out!